by Kevin McCormick

The Federal Reserve was created in 1913, prior to World War I, in conjunction with the federal income tax. The income tax serves to circulate and redistribute money in the economy and to provide credibility for the federal debt, and the federal debt also supports the speculative financial markets, but that is another topic.

The key feature of the Federal Reserve Monetary System is that money takes the form of bank deposits which are created as loan proceeds. Nearly all money transactions are conducted through a "payment system" in which sums are subtracted from one bank account and added to another. In this way bank deposits fulfill the functions of money. In simple terms, a commercial bank makes a loan by adding the loan amount to the borrower’s bank (deposit) account. In practice, most loans require collateral, such as a house, automobile, or business asset as security for repayment of the loan. Often the loan proceeds are paid directly to the seller of the asset (to the seller’s account) and not actually added to the borrower’s account, such as in the “closing” of a house or auto purchase or a credit card sale. This deposit money did not exist before the loan was funded, so the commercial bank created the money through account entries. Thus, commercial banks control the creation, issuance, and use of new money.

The bank loan requires repayment of principal and interest. The principal payments reduce both bank assets and deposit balances. The interest payments also reduce deposit balances but are transferred to the bank’s account and spent by the bank. The money for the interest is not created in the initial loan process but instead must come from money created by other loans and circulated in the economy. However, other bank loans are not sufficient because they all suffer from the same limitation — not enough money is created to pay the principal plus interest on the loan.

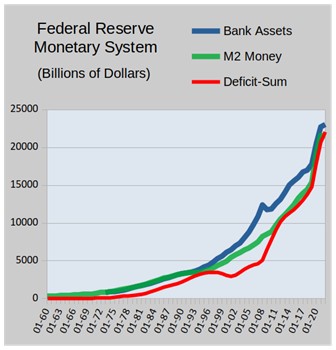

The accompanying chart suggests the source of the necessary additional money is the federal deficit. The federal government borrows money by issuing treasury debt and then spends that money into the economy through government payrolls, military spending, medicare, and other government programs. Since the deficit is borrowed, at least a portion can be newly created money from the commercial banks (facilitated by the Federal Reserve in secondary markets). Federal spending results in replenishing the private deposit accounts that have been reduced by loan payments, making the creation of new loans and deposits possible since the borrowers remain creditworthy. If the federal government balanced its budget and avoided a deficit there would be no money creation outside of the commercial bank and borrower network and many borrowers throughout the economy would be unable to make their loan payments, possibly resulting in a credit contraction and deflation. The federal debt compensates for the shortage of deposit money and allows monetary inflation through debt creation. Monetary inflation is often referred to as “economic growth” and is a constant fixation of corporate and political propaganda.

The chart shown uses data from the St. Louis Federal Reserve Bank. Note the close relationship between Commercial Bank assets (loans), the M2 money supply (deposits) and the accumulated federal deficits. The process begins with a commercial bank loan creating a deposit, then loan payments reduce the deposit account, and continues with the federal government borrowing and spending enough money to replenish the deposit balances counted in M2. The federal debt grows — with an ever increasing interest expense. To create money for interest payments the total debt must constantly increase. The chart shows the increase is approximately 7% compounded annually, which means the sums will double about every 10 or 11 years. The inflation is reflected in real estate and other asset prices, in increasing consumer prices, in the boom-bust credit cycle — basically wherever in the system conditions allow price increases.

The system is rather haphazard since there is usually no assurance that any given borrower will succeed in acquiring the money for debt payments. This is reflected in a competitive culture, pervasive economic insecurity, onerous debt obligations, great inequality, and periodic bailouts of privileged corporations.

In summary, commercial banks direct economic activity for their profits by creating loans and deposits. The deposits make up the money supply. The money supply is reduced by debt payments. The federal government issues treasury debt to borrow money that it spends into the economy, which maintains the money supply allowing borrowers to continue making payments and banks to create new loans and deposits, and thus inflate the monetary system. The income tax assures that interest on the federal debt will be paid. Needless to say, the federal debt itself will never be paid because to do so would deflate the monetary system.

This article has attempted to describe the basic design of the Federal Reserve Monetary System. As Michael Rowbothem states: this is a monetary system that actually operates in its own detached and limited mathematical world and which projects its own versions of the facts. The Grip of Death, A study of modern money, debt slavery, and destructive economics. Jon Carpenter Publishing, 1998.

Chart data references:

- Board of Governors of the Federal Reserve System (US), Total Assets, All Commercial Banks [TLAACBM027NBOG], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/TLAACBM027NBOG, July 24, 2023.

- Board of Governors of the Federal Reserve System (US), M2 [M2NS], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/M2NS, July 24, 2023.

- U.S. Office of Management and Budget, Federal Surplus or Deficit [-] [FYFSD], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/FYFSD, July 24, 2023